Project Finance is a specialized finance discipline that has played a key role in the development of large scale infrastructure, including roads, highways, and even water and energy projects, such as Oil & Gas investment, renewables, and hydroelectric dams.

Learning project finance will set you apart as a financial and data professional because you will play a key role in large-scale deals that typically span multiple stakeholders, such as lenders, equity investors, government regulators as well as technical companies. Project finance is also a highly stable field, given that we always require new large-scale investments as well as maintenance and renewal of old infrastructure.

This is the best time to learn project finance because its scope is diversifying. Trends are changing and evolving with AI and other non-traditional sectors and asset classes that are starting to implement project finance investment principles into their game. These include power generation, midstream assets, innovative long-term offtake energy agreements such as virtual Power Purchase Agreements (PPA) that take place between power generators and buyers. Industries that typically raised on balance sheet debt such as semiconductor, financial services, telecom core networks, electric vehicle, battery storage and distributed energy and antenna-system investments are moving towards project finance to de-risk and focus solely on the project cash flows.

Digital infrastructure will continue to grow enormously with companies needing more and more power and energy to meet consumer demand for AI and cloud computing services. This is a new asset class in project finance, where MORNINGSTAR, a well-known finance rating company, rated the first project finance private placement in hyperscale data centers in the US. Institutional investors such as pension funds and private insurance companies that invest in assets to maintain growth and liquidity in their portfolios are becoming more comfortable to lend money in data centers project-finance backed projects.

As an analyst, you will also learn how to forecast revenues and give a professional opinion on the risk that different financial metrics pose to the project. For example, Morningstar analysts state that for data center financing, one core metric is lease churn. That means, at which rate do “tenants” (those who rent IT servers) stop using the leasing service and how easy is for data center companies to acquire a new customer? Well, according to them, lease churn is increasing and poses higher level of uncertainty. These types of insights are the ones you can learn through PF analysis.

With this, I made an important point about project finance. Project finance (PF) allows sponsors–which are the instigators of the project that needs financing–to raise higher levels of debt in the project capital than they would otherwise be able to. Lenders have limited recourse and sometimes no recourse at all. But what is recourse and why should we care about PF?

Imagine you are an O&G company and you want to invest in a new project with a technology that you have not used before but according to your analysts, it has proven commercial viability and a large upside earnings potential. The challenge you encounter as a company advisor is that you are not able to raise the necessary debt you need to finance the project because you are already highly leveraged.

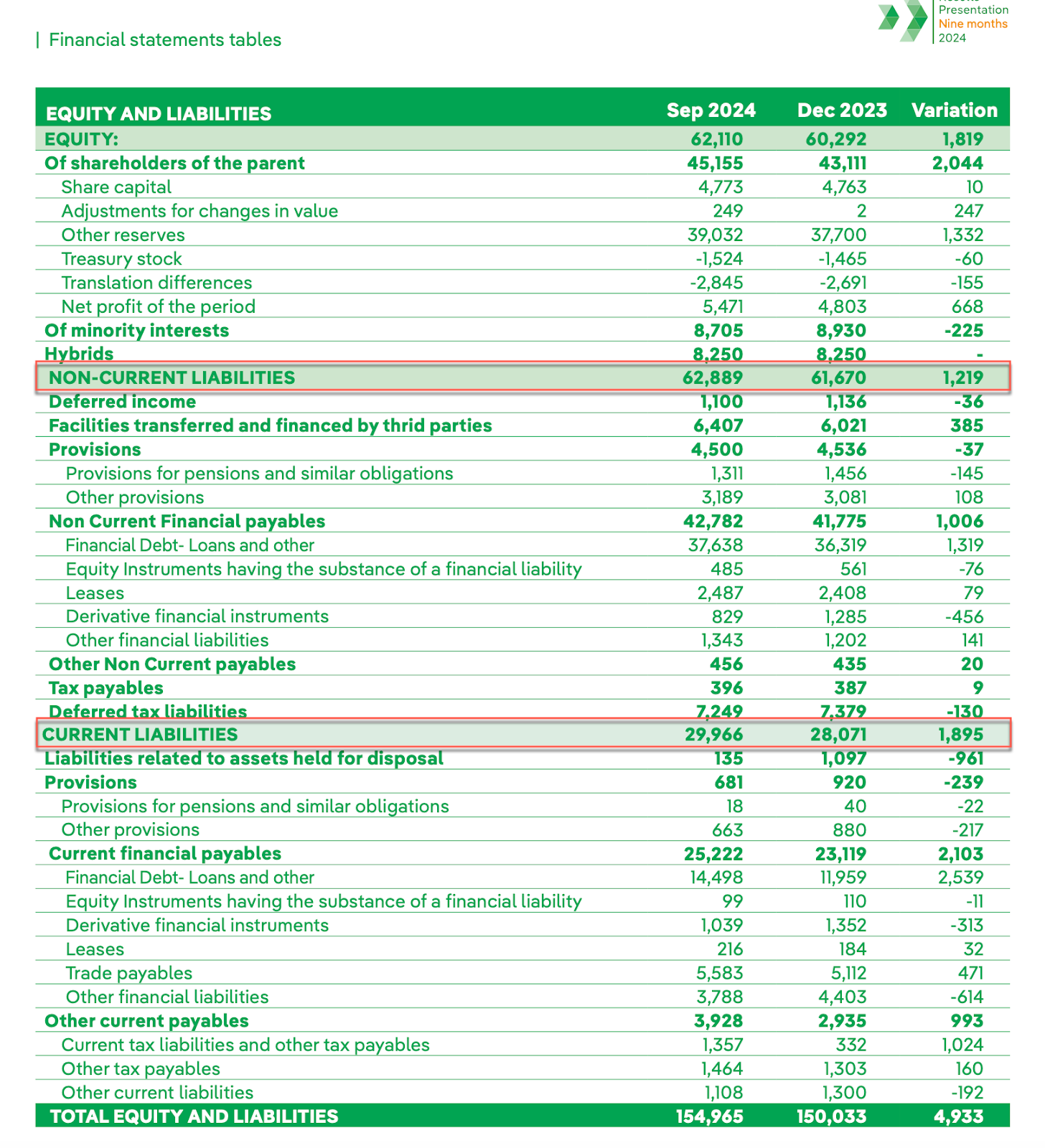

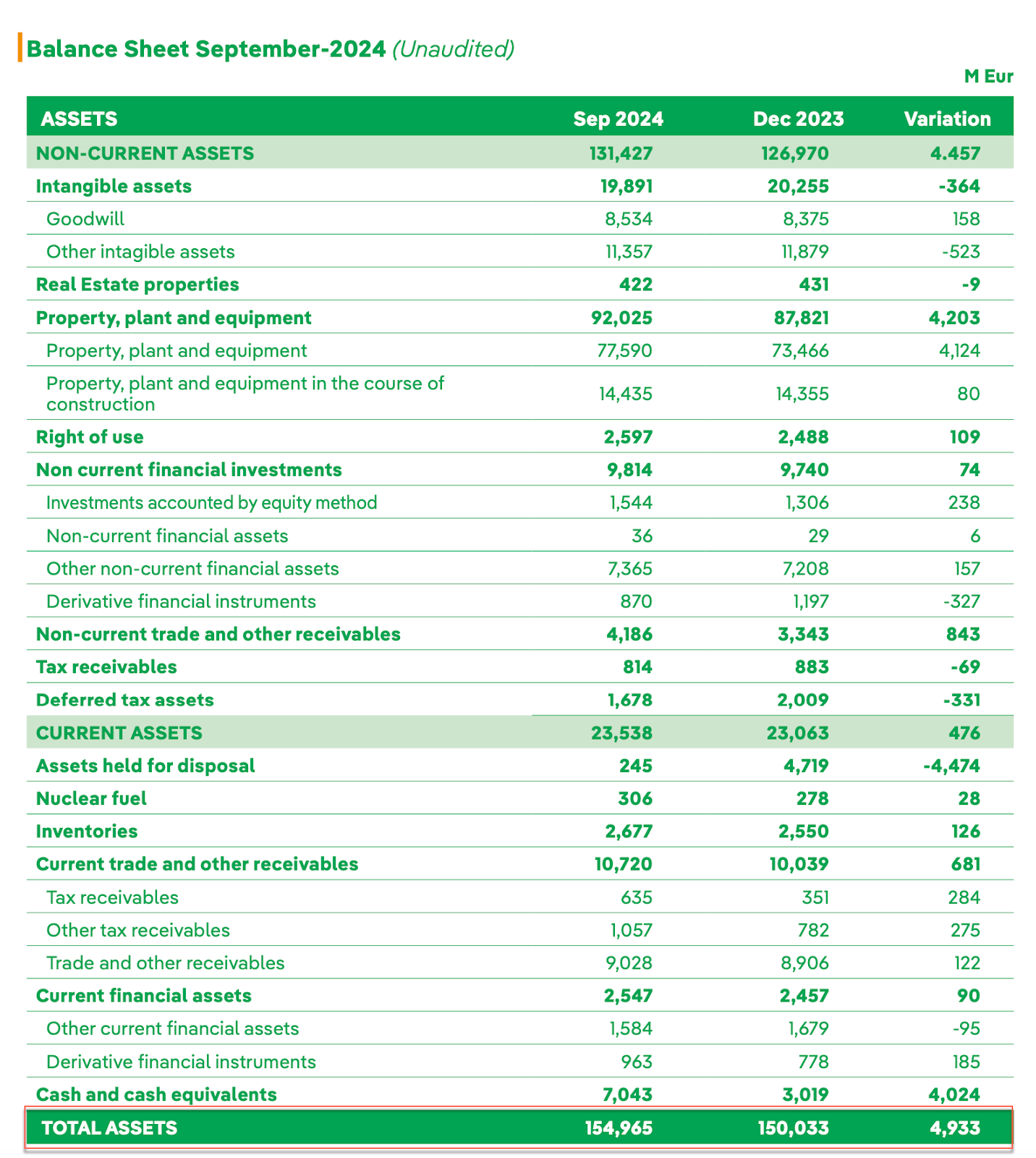

Let’s take Iberdrola, S.A., a well-known Spanish energy utility company as an example. Iberdrola has a wide energy revenue-generating portfolio in many countries, including Spain, UK, Brazil and Mexico. If we measure the company’s total liabilities to assets ratio (as of September 2024) based on the 9-month results presentation on their website, which is:

- Current liabilities (EUR 29,666 m) + Non-current liabilities (EUR 62,889 m) = EUR 92,555 m of total liabilities

- Total asset value (EUR 154,965 m)

- Total liabilities to asset ratio = 61.6%

We obtain a value of 61.6%. Is this high or low? It depends. Can you compare this value to other peer companies operating at Iberdrola’s scale? Does Iberdrola face cash flow issues? How competitive are the historical returns of investment compared to the effective interest rate that the company must pay? All these questions and analyses must be done before deciding whether PF is a good option or not.

Bondholders also place conditions when lending money to corporations. These conditions include not taking more leverage than a certain threshold, for example: “Your debt-to-asset ratio cannot be higher than 50%”. These kinds of clauses are known as “covenants”. Trust me, every bond issuance (i.e. borrowing money) comes with a large amount of covenants that require legal, financial and operational expertise.

If the company that wants to sponsor a new large project does not want its corporate balance sheet results to be negatively affected (due to incurring more debt), it can decide to create a special purpose entity (SPV) which is a legally independent economic vehicle that allows project raise the amount of equity and debt necessary for the completion of the project, without sacrificing its own core balance sheet metrics or ratios. In those cases, the SPV company will issue debt and mezzanine equity to finance its project. Bondholders and equity investors will scrutinize and assess the cashflow potential of the project in order to decide whether it’s worth the risk or not.

If lenders see a high upside potential, meaning that, not only debt will be easily covered and serviced, but also there will be plenty of operational cash flow available; it is more likely that they will lend more money at a lower interest rate.

Going back to the question: what is a recourse? Well, you probably know that if you don’t pay back your mortgage, the bank is likely to take over your home and sell it to pay off your debt. In PF, lenders have little recourse from the sponsor’s assets. That means, if Iberdrola creates a legally independent SPV, and the project does not work as expected, lenders will not be able to take Iberdrola’s assets to service their debt.

That’s why in PF there are key ratios and covenants that monitor the financial health of the project. Sometimes these ratios are advised but at other times these are mandatory and must be respected. An example of such ratio is the debt service coverage ratio. Under this ratio, the sponsor must be have enough operational cash flow available to service their debt principal and interest payments. This is typically expressed in a ratio, where the higher the ratio, the better and safer lenders feel about their money. In PF, these contracts can range from 1.25x to even 2x.

Another aspect of PF is that risk tends to be allocated equitably across parties. PF deals can get easily complex and messy, with dozens of stakeholders being involved. Let me give you a clear example. For toll road projects, projections are made for the usage of toll road and the minimum number of users needed to make the project profitable. Have you ever been on a toll road that seems to be empty and almost not used at all? How do sponsors repay their loans if the construction ends up not being used at all? Insurance and back-up guarantors are sometimes needed to make up for cashflow shortfalls. Government agencies and institutions might provide additional funding to sponsors if some usage metrics are not met and therefore operational cashflows are lower than expected. This occurs because the construction of a road was mandated from the government and as part of their security and logistics campaign for rural users, for instance.

Public goods are not always profitable. Airports built to connect areas that are of strategic importance but there is a low consumer demand might result in financial losses and still use project finance.

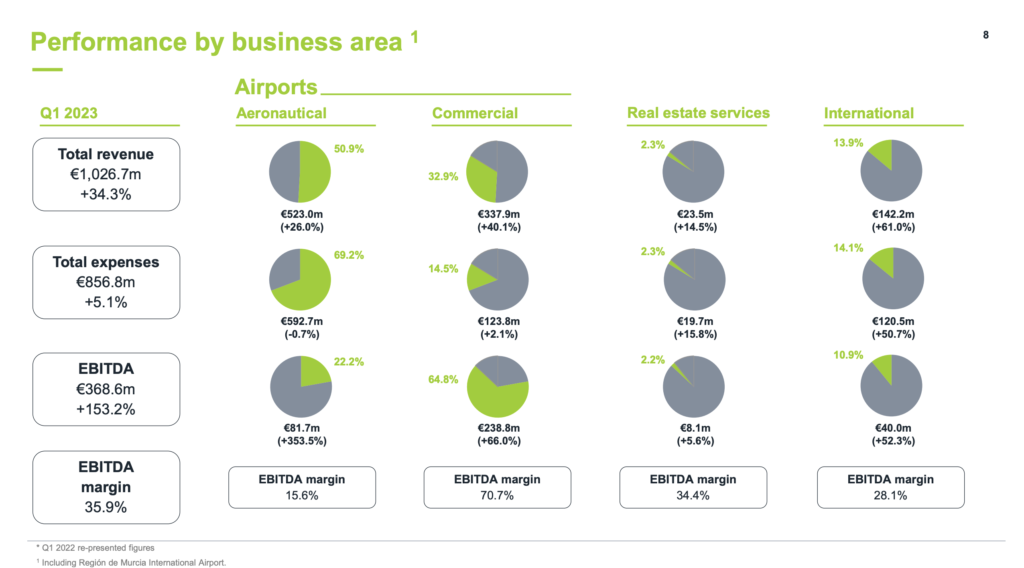

I’d like to share with you as well the results from AENA, which is an airport facility company that operates in Spain and internationally. In this slide, they present their performance by business area. As you can see, commercial airport revenue have the highest EBITDA margins (with around 70.7%) from its business segments, which contrasts to aeronautical airport revenue with only 15.6% of EBITDA margins. Commercial revenues stem from retail store rentals, restaurants and food courts, parking fees and car rental concessions as well as advertising whereas aeronautical revenue comes from landing fees, aircraft parking fees, terminal usage or ground handling services. The more maintenance needed, the higher the operational expenses and the lower the EBITDA ratios.

In PF, collaterals are also used to reduce the risk of lending. Since recourse is limited, lenders may require more collateral and higher financial ratio forecasts to offset the higher risk. Collateral is given by sponsors to lenders as security for receipts and examples include the assets tied up in managing the project.

In conclusion, project finance stands out as an exceptionally rewarding career path that offers both intellectual and financial benefits. The field’s complexity, combining elements of finance, law, engineering, and risk management, creates high barriers to entry that help maintain strong compensation levels across the industry. What makes project finance particularly attractive is its crucial role in developing essential infrastructure – from renewable energy projects to digital infrastructure – that shapes our modern world. The sector’s growing importance in addressing global challenges like climate change and technological advancement ensures sustained demand for skilled professionals.

Iberdrola Statements (September 2024 9-month results):